However, the house or property need see Va lowest assets requirements inside for every condition. The proper agent can ascertain what things to get a hold of and certainly will functions physically together with your financial to make certain your Virtual assistant loan schedule stays focused.

step 3. Going Below Offer

That have a dependable representative as well as your Virtual assistant financing preapproval page, its just a question of big date before a supplier allows your own buy promote. Getting your offer recognized is commonly referred to as getting “less than price,” as it’s the specialized kickoff to invest in transactions between your client and provider.

Getting your provide recognized is excellent information and worthy of honoring, but you may still find a few methods remaining until you can be telephone call our home your:

- Display your package details with your lender

- Order property inspection (recommended)

- Get lender buy an excellent Va appraisal

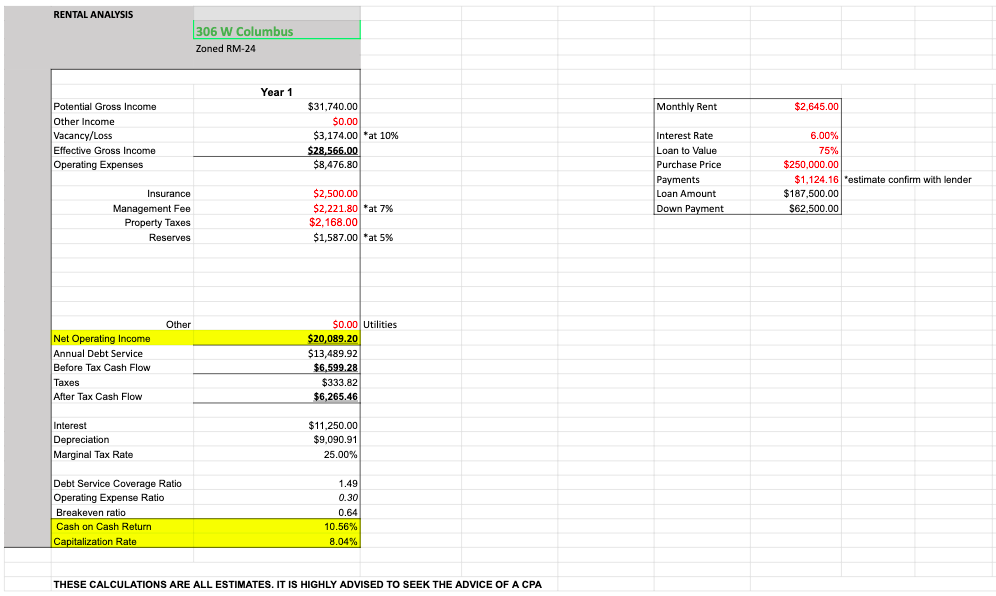

At this point, your own financial will be give you a better thought of exactly what closure can cost you and you can fees can be expected, such as name or financing costs. There are even particular low-deductible fees you to definitely Virtual assistant consumers usually do not shell out. Certain buyers also query suppliers or loan providers to cover a number of these closing costs as part of lingering deals.

When you are sorting from buy agreement https://paydayloancolorado.net/sterling-ranch/ info on provider, your own financial tend to move ahead to the next step regarding Virtual assistant mortgage schedule-underwriting.

cuatro. Virtual assistant Financing Underwriting

Your own lender will begin the new homework to be sure you can spend the money for home from the rates revealed of your house deal.

Generally speaking, lenders apply an automatic Underwriting System (AUS) to assess a beneficial borrower’s creditworthiness easily, streamline the mortgage recognition process, and reduce the likelihood of human error. They will certainly plus most likely have fun with a keen AUS after you apply for preapproval.

But not, particular consumers with unique financial affairs, such as those no credit rating, is almost certainly not passed by an AUS. In the event that a keen AUS denies you, it is far from the conclusion the street.

You could consult manual underwriting, which is whenever a human underwriter requires a closer look at debt character. This action requires offered but could end up in a far more good results into borrower.

This new underwriting group tend to wait for Va assessment prior to signing the loan document and you can granting an effective “obvious to close.”

5. Closing toward good Virtual assistant Mortgage

Closing on the financial is a significant achievement, and the Va mortgage closure timeline is very similar to most other home loan closings. They begins with your Closure Disclosure.

Regulations necessitates that you get a closing Revelation out of your financial about about three business days prior to the loan closes. Your own Closure Revelation will show what you would owe to your closing time, if anything, including:

- Advance payment

- Representative fees

- Name costs

- Most other closing costs

The financial have a tendency to feedback that it document with you and you may respond to any questions you have got you is totally familiar with exactly what you owe and why. People have a tendency to do a final walkthrough of the home ahead of closing to ensure things have stayed the same just like the heading significantly less than price.

What to anticipate towards the Closing Go out

An ending big date fulfilling may take 1-couple of hours, according to the nature of one’s get arrangement amongst the consumer and seller. However, it’s necessary so you’re able to take off more time as safe and need your own time looking at the fresh new documents.

Anticipate to signal your final documentation. Your name providers tend to take you step-by-step through for every part of the closing records they will have wishing on your own additionally the seller’s behalf. In the event that records come in acquisition, might afford the down-payment harmony, if any, plus display of one’s settlement costs.