Income Severance loans for bad credit stability is key outline underwriters think whenever evaluating home loan software. If you are employed, meet with the lowest borrowing from the bank criteria and secure enough income, you can suppose you’re a fantastic candidate getting a home loan. But quite often it requires over that have a job to complete one of the largest sales of your life. You should also have proof reliable, continuous earnings in advance of you may be accepted for resource.

When you are happy to get a mortgage, here’s what a lending company actively seeks whenever choosing if your revenue qualifies to be secure.

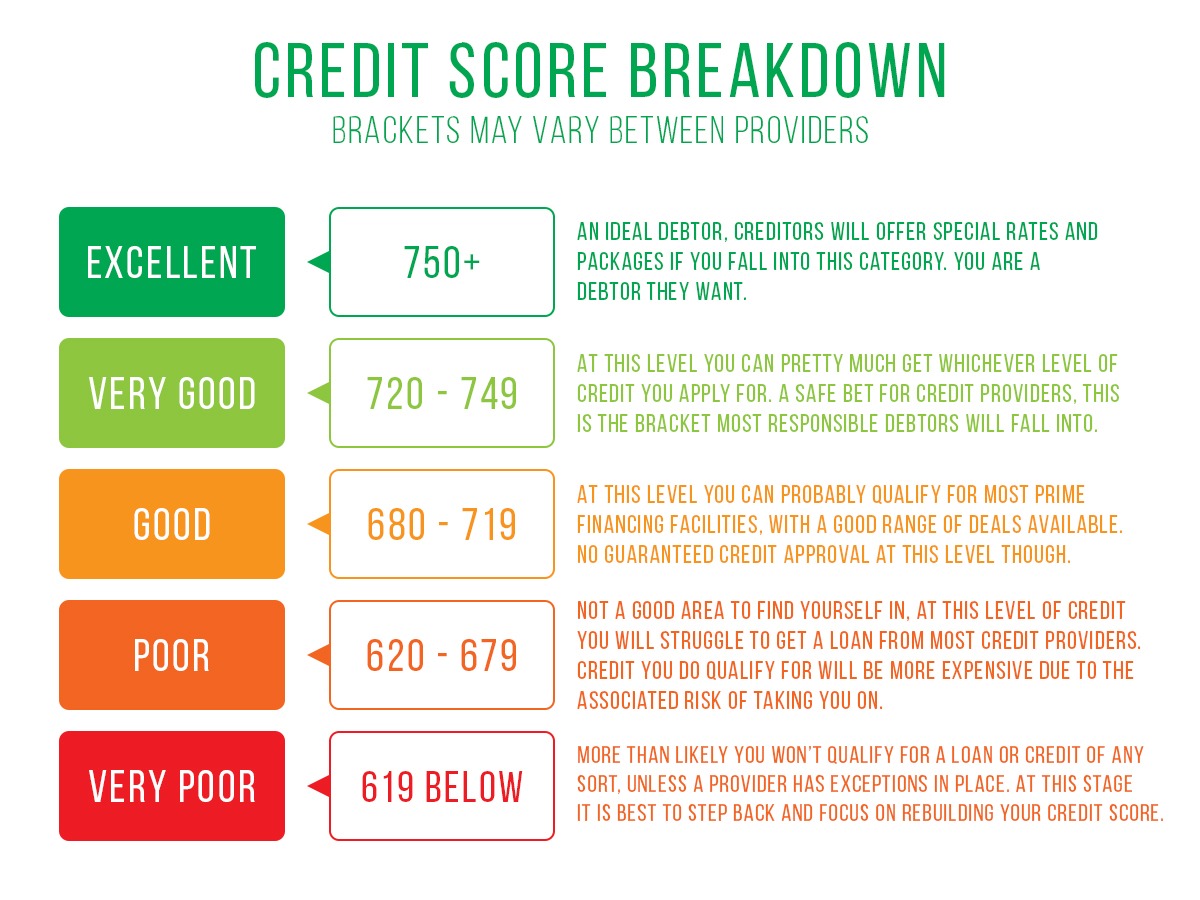

Revenue stream

Balance of cash happens hand-in-hands with a position. But being qualified to possess a home loan involves more being employed and receiving a salary. The precision of income including takes on a vital role. Since the a mortgage was an effective fifteen-, 20- or 30-12 months partnership, your own lender must indicate the cause of one’s money, and size your capability to keep up this income enough time-title.

The good news is, income pointers published to a loan provider to possess qualifying objectives actually restricted so you can earnings gotten regarding a career. Other acceptable earnings sources tend to be loans you get of advancing years withdrawals, permanent disability, youngster assistance, and you will alimony, etcetera. Some loan providers also allow it to be money of the next jobs when qualifying home loan programs. Before you include additional earnings otherwise money of supply other than just employment, you ought to in addition to inform you convincing facts that the earnings continues to the foreseeable future.

Such as, if you wish to is youngster assistance otherwise alimony payments your found whenever being qualified for a home loan, such costs have to continue for at the least 3 years in the day of your application, and you also ought to provide noted proof of the assistance agreement. Furthermore, one which just were earnings away from an additional jobs, particular lenders tend to consult records to verify a single- to help you a couple of-season history of operating multiple perform. This may involve tax returns otherwise income stubs.

A job Gaps

If at all possible, don’t have a position gaps 24 months just before applying for a mortgage. It is because lenders prefer people who have been utilized for at the very least 24 straight weeks. Definitely, lives will not always go according to plan. And often, we find our selves suddenly underemployed. A space into the employment would not result in one particular home loan rejection, but you will need give an explanation for points around this pit.

Their financial commonly ask for factual statements about your hiatus. Do you rating laid off from your work? Did you bring prolonged pregnancy get-off? Do you prevent your task doing a diploma? Did you experience a disease or injury? Did you look after a sick cousin?

Because there are no tough otherwise quick statutes out-of a position holes when being qualified to have home financing, just your own financial can decide whether you match the brand new criteria to possess home financing acceptance immediately following experiencing the reasons.

A couple successive numerous years of work also applies if you find yourself a home-operating borrower. It can be challenging to be eligible for a home loan once the a self-employed borrower, however it is maybe not hopeless. You need to promote 2 years regarding providers tax statements. In many instances, lenders make use of the mediocre of income (after company expenditures) for the past couple of years to choose your being qualified count.

Jobs Hopping

But then, maybe you don’t possess work openings, however, you have presented a cycle off jumping from occupations in order to a special. When deciding the soundness of money, loan providers and additionally account for just how long your are nevertheless having employers. Changing companies on a yearly basis or all of the two years would not fundamentally stop you from delivering a home loan. However, for your money to help you be considered given that secure, work change has to take set into the exact same field, and with per change, your revenue must will always be an equivalent otherwise boost.